Fees critically matter for evaluating investment returns. Index fund pioneer and Vanguard founder, John Bogle, said, “You get what you don’t pay for.” His message: minimize fees. In September 2014, I gave a talk at the “Who Will Own the Forest?” conference in Portland, Oregon specific to this theme as it relates to timberland investments. Institutional investors asked conference organizers about a perceived misalignment of timberland management fees relative to prospective timberland returns. My comments focused on addressing, “well, what does the “data” say with respect to this perception?”

Timberland Investment Returns

First, let’s remind ourselves how timberland investments, broadly defined, performed during the recent economic chaos. During the ten-year period from January 2004 through December 2013, annualized returns for timberland investments outperformed the broader stock market.

Direct timberland ownership, based on the U.S. NCREIF Timberland Index, generated annualized returns of 8.4%. Ownership of shares in timberland-owning REITs, based on the Forisk Timber REIT (FTR) Index, generated annualized returns of 9.4%. During this same period, the S&P 500 returned 5.2% annually. Basically, timberland investments provided the desired stability and diversification through a distressing economic cycle.

Timberland Investment Fees

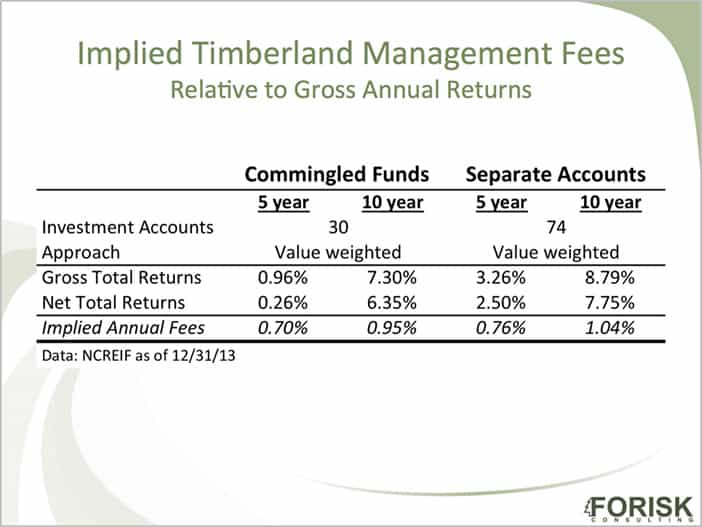

The fees and costs differ for direct timberland ownership versus shares in public timberland-owning firms. Reported returns from public timber REITs, as with any public stock, already account for “management fees”, while those associated with private timberlands as reported by the National Council of Real Estate Investment Fiduciaries (NCREIF) normally do not. However, in the past few years, NCREIF began reporting fund level “gross” and “net” returns that allow us to estimate fees paid for timberland asset management services.

The table below includes data from 11 TIMOs covering 11.9 million acres of private timberlands in the United States. The analysis separates commingled funds, which pool investments from multiple investors, from separate accounts, which manage funds from specific institutions separately. The “net” returns subtract all investment management advisory fees, including paid and unpaid performance incentive fees.

The implied annual fees are consistent with Forisk analysis of prospectuses and contract structures, which find that TIMO incentive pay representing an “overage” or “carried interest” of 10 to 20% above a hurdle of 7 to 8% nominal is common. In addition, the implied fees are consistent and in line with ranges reported by consultants at Mercer for other non-timber asset classes. Specific to timberland, Forisk research found average total fees from 2005 through 2012 of 84 basis points (0.84%).

This content may not be used or reproduced in any manner whatsoever, in part or in whole, without written permission of LANDTHINK. Use of this content without permission is a violation of federal copyright law. The articles, posts, comments, opinions and information provided by LANDTHINK are for informational and research purposes only and DOES NOT substitute or coincide with the advice of an attorney, accountant, real estate broker or any other licensed real estate professional. LANDTHINK strongly advises visitors and readers to seek their own professional guidance and advice related to buying, investing in or selling real estate.

I would like some help in determining whether to keep my only 200 acres of timberland or sell it. I do have about 95 acres of pastures sourrouding it and am getting an income from that. Some farmers want to buy the pasture but I insist they must buy half of the timber with it. I could keep an easement into the timberland.

My timber was cut approximately 6 years ago down to 12 ” . It had not been cut prior to that for many years. How do I determine what it is accrueing at this point – from my net at that time of cutting or perhaps a lesser amt because there were some trees that were 60 yrs. old -not growing too much after 30 I understand however.

Can someone help me with figures and whether it would be more profitable for me to sell.

Phyllis- Where is your property located?